Have you ever experienced working, working, and working for nothing?

Every time you receive your paycheck, almost nothing is left! You pay for your rent, utilities, phone bills, and your DEBTS and what is left is just your daily office allowance just enough to pay for the commute and cheap lunch.

And you don’t understand why this Cycle of Earning and Paying Debts doesn’t end! You received an increase in pay but the debt doesn’t end! The bible is correct in saying that “The Borrower is SLAVE to the LENDER”.

The Outer World is a reflection of our Inner World

Debt is often the result of bad habits. And the causes of these habits are negative mindsets we believe in, consciously or subconsciously. One of my mentors, T. Harv Eker, always say that your physical reality is the result of your inner reality.

Debt is often the result of the following mindsets:

1. I should always be up-to-date or I will not be loved.

You are loved because you are loved. You don’t need to prove yourself to other people. Your real friends should accept you as you are. Your family should love you as you are.

You don’t need to go into debt just to prove yourself to other people and for them to like or love you. If people around you can’t accept the real you, then it’s time to move on and find real friends to be with.

When you are tempted to use your credit card or go into debt just in order be up-to-date and be loved, always remember this quote from the movie Fight Club:

2. It’s okay to go into debt for my loved ones.

Getting into debt because of family and friends is not always okay. A life and death situation is a different issue but going into debt just to please the whims of our loved ones is just simply wrong.

Your loved ones should be the first people to understand your real situation. The key here is being open to them and explaining to them your circumstances. People who really love you and care for your will not want you to be in the quicksand of debt.

When it comes to giving gifts, always remember that what is important is the thought and not the price. Never go into debt just to make your loved ones happy and make yourself “happy”.

The feeling of satisfaction and pride of giving an expensive gift will only last for minutes or days but the pain of paying the debt will last for months or even years. People who truly love you will value your company more than your gifts.

3. I work hard and I deserve to enjoy life! #YOLO!

Yes you work hard and you deserve to enjoy life. You only live once! And if you live right, once is already enough. So when it comes to your expenses you should live right.

If you will only live until today, it is okay to go into as much debt as possible. But you will not only live until today and Retirement Is Not As Far As It Seems. It is okay to spend for enjoyment as long as it is within your budget or what I call your Play Fund.

How not to be in Debt?

Now that you know the mindsets that place people in the shackles of debt, below are 3 Tips of CommonCentsPH on how not be in debt.

1. Have a Budget

I don’t care if you are earning billions, millions, or thousands, if you don’t live in a budget, you will always blow up your finances. Remember, the Ultimate Measure of Wealth is not income but net worth (assets – liabilities).

Do you know how much you earned and spent last month? If not, it’s time to track it. I use the app Spendee for this. There is saying that what gets measured gets done.

The most common budgeting guideline is the 70-20-10 Rule. It says that your living expenses should be 70% of your income at most. At least 20% of your income is saved and invested. And the remaining 10% is for tithes or charity.

What I use is T. Harv Eker’s Budgeting Jar which goes like this:

- 55% – living expenses

- 10% – Financial Freedom Fund (this is for retirement, business, investments)

- 10% – Long Term Saving for Spending (House, Car, Big Travels, etc.)

- 10% – Educational Fund (use this is increase your knowledge and skills)

- 10% – Play Fund (shopping, dates, movies, travel, etc.)

- 5% – Give Fund (charity, church, and helping others)

With this formula, it is easier to live within your means. The play fund can be saved up to 3 months max but should be ideally used monthly. If you are not enjoying life for the next 3 months, you will most likely blow up your budget on the 4th month because you will feel that you are being deprived which might result to debt through spending spree.

So the next time you want to travel abroad, which will worth P100,000 but the 10% of your monthly income is just P5,000,it means that this can’t be used for your Play Fund. The maximum amount the Play Fund can be accumulated is P15,000 (P5,000 x 3 months). After reaching that point, it should be used!

Hence, the P100,000 travel should be treated as a Long Term Saving for Spending (LTSS). With a P5,000 LTSS Fund per month, you should wait for 20months before traveling abroad (P100,000/P5,000 = 20months).

This will result to better travel because this is a travel that you can really afford and do shopping spree because it is budgeted and not a result of debt. I believe this concept is better than traveling for 5days but being in debt for the next 24months! Delayed Gratification is key!

2. Have Short, Medium, Long Term Goals!

When you have a goal, you won’t care what people will think because you are focused on your goals. A short term goal is seen to be achieve within the next 2 years. A medium term goal is seen to be achieved in the next 3-10 years. A long term goal is 10 years above.

If you have read the stories of successful businessmen and tycoons, they lived below their means. They don’t care if they take public transport, bring packed lunch, and miss parties. They believe that if they can delayed their gratification and achieved their dreams, they can enjoy life everyday without thinking of money in the future.

So the next time you are tempted to swipe that credit card always remember that you have a budget and you have goals! And say this to yourself:

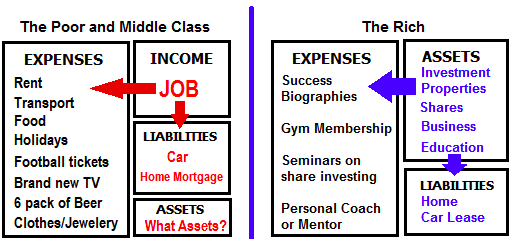

3. Know what is an Asset and what is a Liability!

Robert Kiyosaki defines an asset as something that places money in your pocket while a liability is anything that takes money from your pocket. One of his most controversial statements is that your house is not an asset! But is it?

People say that it is best to invest in real estate because it is the asset class that doesn’t go down. If you buy a house and live in it, will it give you money or take money from you? Isn’t it that you pay electric and water bills, repairs, association dues, and real estate taxes for your house? By the definition stated above, it is a liability.

But let’s say that you bought a house with the intention to rent it out for P30,000 per month. Yes, you pay taxes, association dues, repairs, and a person to take care of the house but the net income you get is P20,000/month. With our definition, then this is an asset.

With this mindset, you may now be more prudent and intelligent every time your purchase things especially from your LTSS. Below is the difference how The Poor and Middle Class and The Rich spend:

The rich buy assets that will pay for their expenses. The Poor and Middle Class spends their income to purchase liabilities. In the end, the poor and the middle class can’t stop working. The rich can stop working and enjoy life because their assets are the ones that pay for their expenses. The rich continue to work because of passion and purpose and not for money.

I am Drowning in Debt and I need Help!

If you are drowning in debt, don’t lose hope! With the right strategy and discipline, you will be debt-free and financially free in the future!

When it comes to getting out of debt, no one can help you but yourself!

Here are CommonCentsPH 5-Step Guide towards being Debt-Free:

1. Have A Budget

While creating a budget, identify your needs and wants. Eliminate all the wants that can be eliminated and what lifestyle change you can do for the mean time such as taking public transport, bringing packed lunch, and skipping parties and drinks.

Sacrifice is needed if you want to get out of debt! You are not in the position to ask for a balance life until your bank account is balanced. This is the price you need to pay for!

2. Find Ways to Increase Your Income! And Increase It Fast!

To pay your debts faster, you need to increase your income and increase it fast. It can be achieved through part-time work, over-time, and selling things. Avoid going to “businesses” that will ask you to invest a large capital and will place you into further debt. You should be as conservative as possible while you are in debt.

3. Pay the Easiest to the Hardest Loan! Always Pay the Minimum!

If you have multiple loans, pay the easiest to pay first! This will give you a sense of accomplishment and progress! But don’t forget to pay at least the minimum due amount for the other debts because the finance charge is larger than the interest charge.

4. Consolidate High Interest Loans To Lower Interest if necessary!

This part is a bit tricky and you need to crunch the numbers for this. Let’s say that your outstanding amount due for Credit Card A which charges 3.5% per month is P50,000 and for Credit Card B which charges 5% per month is P250,000.

Your budget per month for your credit card debts is just P10,000. What should you do?

Credit Card A charges you at least P1,750/month in interest while Credit Card B will charge you you at least P12,500/month in interest. That is a total of P14,250 minimum payment per month interest charge!

But you can only afford P10,000/month. If you don’t pay the minimum the credit card company will charge you 7.5%/month of the balance due. This will result to a snowball and will further drown you deeper to the quicksand of debt.

My suggestion for this is to consolidate the loan to a credit card company that will offer lower interest rate where you can pay P10,000/month. They will tell you how many months you need to pay with the said amount with no longer incurring additional interest and finance charges.

Once the plan is set, don’t incur additional debt and stick to it until you are debt free! It is also best to consult a wealth planner or a debt specialist for this.

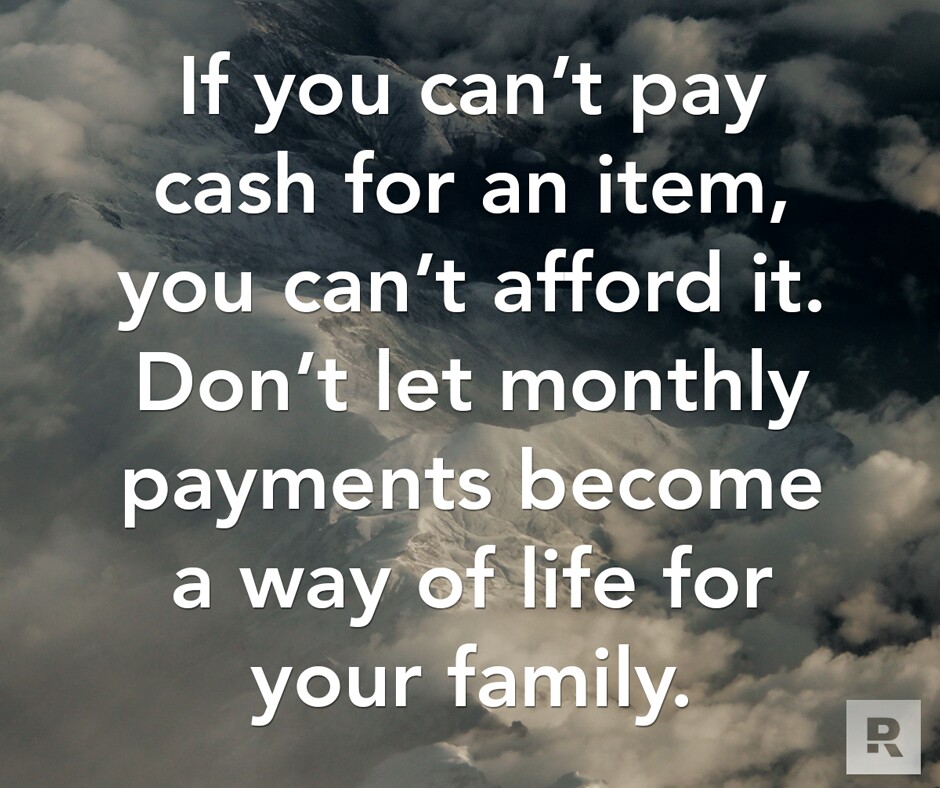

5. Pay Only in Cash

Only buy what you can afford. If you can’t pay in cash, you can’t afford it.

How about big purchases such as appliances and gadgets? Isn’t it where all this debt problem started? Purchasing big amounts is where LTSS comes in — budget your way through it.

Congratulations You Are On Your Way Towards Being Debt-Free!

To summarize, always remember the following:

- Your physical reality is the result of your inner reality. You are good as you are. No don’t need to prove yourself to anyone.

- Have a budget and set goals. Having financial goals will make you stick with your budget and prevent you from being debt.

- To get out of debt faster, eliminate your wants and find ways to increase your income so you can pay your debts as fast as possible. Stick to the plan! It is the price you must pay! Always remember: If you can’t pay in cash, you can’t afford it.

Every time you go to work, always tell yourself that you work to Build a Future and not to Pay for the Past!

Your Millennial Wealth Planner,

Harold Q. Gardon, CWP, CEPP

How do you find the article? Do you have any questions? Please feel free to message me if you want me to discuss a particular topic or if you are seeking financial advice.

How do you find the article? Do you have any questions? Please feel free to message me if you want me to discuss a particular topic or if you are seeking financial advice.

Subscribe to my mailing list and get a FREE copy of my e-book entitled “Millennial: A New Definition of Wealth”

We can also keep in touch through my FB Page.