Do I still need a VUL Plan if I already have an online stock trading account?

Is there a difference between the two?

Aren’t they the same? Both have investments right?

The answers are YES and NO.

YES, they both have investments.

But NO, they are not the same.

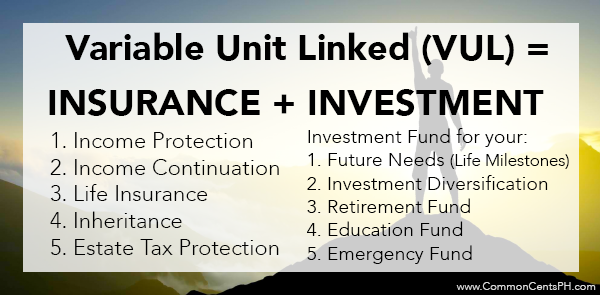

VUL Simply Defined

Variable Unit-Linked or VUL for short is a life insurance product with an investment component.

It’s main purpose is to provide protection for you and your family against life’s uncertainties such as:

Premature Death – VUL makes sure that your dependents will continue to live their current lifestyle. It guarantees that your family will not be poor: that they will have food on the table, roof over their heads, continue their education, etc.

Disability – VUL protects your income in case you can no longer work due to a disability. It makes sure you have enough money to continue your lifestyle and get the necessary medical treatments.

Critical Illness – VUL makes sure that you focus on getting well if cancer, stroke, heart attack, or any other critical illnesses strikes. It makes sure that money will be the least of your worry and that your family does not need to go into debt in order for you to get well.

Poor Financial Planning – since a VUL has an investment component, it can supplement your medium-to-long term savings, kid’s college funding, retirement funding, and the like.

Basically, a VUL makes sure that you or your family does NOT become POOR.

To know more about VUL (click this link).

But Doesn’t My Online Trading Account Makes Sure That I Become Rich in the Future?

Yes, your online trading account may make you rich in the future but it can’t guarantee that you and your family will not be poor.

Let me explain the Financial Pyramid very quickly:

The base of the pyramid is PROTECTION where VUL belongs. Though VUL has an investment component, it’s primary purpose is protection

The base of the pyramid is PROTECTION where VUL belongs. Though VUL has an investment component, it’s primary purpose is protection

Your Online Stock Trading Account is located at the tip of the pyramid that is INVESTMENTS.

When you build a pyramid, you start with the base first and not at the tip. You need to have a strong foundation (base) for the body and tip of your financial pyramid.

Hence, before going into investments you should have protection first and adequate savings (emergency fund).

But You Still Want to Start at the Tip of the Pyramid

So let’s say that you don’t get a VUL and instead you opened an Online Stock Trading Account.

After 1 year of placing P5,000 per month on your account, you already have already invested a total of P60,000 (P5,000 x 12 months) for your trading fund.

And since you are a “savvy” investor, your trading fund value is now at P80,000.

Wow! That’s an incredible investment gain of 33.33%. Not bad for a newbie in the market.

But after 2 days, there were negative rumors about the international market and your investment fund value went down to P50,000.

You know that there is nothing wrong with the fundamentals of the Philippine market and this is just a short-term correction.

And since you do Peso Cost Averaging, you invested an additional P40,000 from your savings.

However, the market continued to go down the next day.

You Fund Value is now at P40,000 but your total investment is at P100,000 (P60,000 + P40,000).

And when you have thought that the worst has already happened, the clinic that does your annual physical exam called you to say that they discovered a cyst in your body and it needs to be extracted to know if it is malignant or benign.

After a week of waiting, the doctor told you that you are very lucky. Though you have Stage 2 cancer, the success rate of the treatment is 90%. However, the total cost of the treatment is P750,000.

You looked at your savings account, it has a little over P20,000.

You checked your Online Stock Trading Account hoping that your money might have doubled. However, it is still a little over P40,000.

What will you do next?

You withdraw your P20,000 from your savings account and P40,000 from your stock account realizing a –P60,000 loss (P100,000 total investment – P40,000 fund value).

And most likely, you need to sell your assets (car, jewelry, etc.), mortgage your house, ask help from your relatives, friends, and government.

Worst of all, you most likely will go in DEBT.

But What If, You Did This Instead…

Instead of investing all your P5,000 per month on your Online Stock Trading Account, you decided to do this instead:

- Place P3,000 on your Online Stock Trading Account, and

- P2,000 on a regular plan VUL that has protection against accidents and critical illness?

If you do this, you won’t be needing to realize you loss on your Online Stock Trading Account.

You don’t need to withdraw from your savings account or sell anything.

You don’t need to ask for help or go into debt.

Because, your VUL Plan will give you at least P1 Million in cash upon diagnosis of critical illness so you can focus on getting treated.

Getting Protection for FREE with interest.

What’s good with VUL is that it has an investment component wherein you can withdraw the money in the future.

And if you start early, the fund value you withdraw will be most likely higher than your premiums paid.

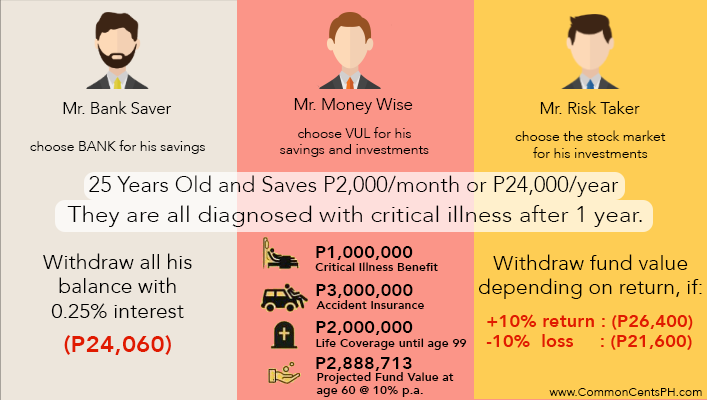

Let me explain briefly. (Let’s assume you are a healthy 25y.o.)

Let’s say your monthly premium for your VUL is P2,000/month or P24,000 per year.

It gives you P2 Million Life Insurance, P3 Million Accident Insurance and P1 Million Critical Illness Coverage.

After 20 years, your total premium paid is P480,000.

The Fund Value of your VUL (amount you can withdraw) at a return of 10% p.a. is projected to be at P704,185*.

*This is not guaranteed is for illustration purpose only. The reader is advised to do his/her own research before investing on a particular investment. Always remember that the higher the risk, the higher the reward.

With this example, you are protected for P2 Million Life Insurance, P3 Million Accident Insurance and P1 Million Ciritical Illness Coverage for FREE for a period of 20 years plus a P224,185 interest from your premiums paid..

It’s just like saving in the bank with a higher interest.

But if something bad happens within those 20years, you make sure that you get protected even if you have just paid a couple of months of premium.

But let’s just say you don’t withdraw the whole amount and you leave P50,000.

Are you still protected? The answer is YES!

You are still covered with P2 Million Life Insurance, P3 Million Accident Insurance and P1 Million Critical Illness and that P50,000 is still invested and can still earn interest for you.

But let’s just say that you plan to pay until age 60, your total premium paid is P840,000 and the fund value that you can withdraw for your retirement is projected at P2,888,713.

You Can’t Build a Pyramid Starting from the Top

In any structure, you need to start from the base.

The higher the building, the stronger the base should be.

Hence, the richer you want, the stronger and deeper is your protection plan should be.

You need to have a solid foundation so when life happens, your financial pyramid won’t go into ruins.

There are a lot of different financial products in the market. And each product has its own purpose.

Hence, it is very important that you are clear with your Financial Objectives once you invest in a particular financial product.

It is also important to have a competent and trustworthy wealth planner to guide you in the process. Find an advisor who has a heart of a teacher than a mindset of a salesman.

If you don’t have a VUL yet, get one as soon as possible.

When it comes to protection, always remember what Shakespeare said, “Better three hours too soon than a minute too late.”

Your Millennial Wealth Planner,

Harold Q. Gardon, CWP, CEPP

How do you find the article? Do you have any questions? Please feel free to message me if you want me to discuss a particular topic or if you are seeking financial advice.

Subscribe to my mailing list and get a FREE copy of my e-book entitled “Millennial: A New Definition of Wealth”

We can also keep in touch through my FB Page.